April 18, 2024

Smart Money Moves: What Bills Help Build Credit?

If you have a lackluster credit history or are brand new to credit, you might be looking for ways to boost your credit score.

After all, that score is often what stands between you and a lot of financial opportunities. For example, if you want to open a new line of credit but have a low credit score, the lender may decline your application. On the flip side, if you want to buy a house and have an excellent credit score, you could secure a more favorable mortgage interest rate.

Luckily, the process of building credit is pretty straightforward: The more on-time payments you make and the lower you keep your credit card balances, the more your credit score will improve over time.

As you kick off your journey to better credit, it’s important to know what bills help build credit to make more informed decisions about your payments, balances, and personal finances. Here’s everything you need to know to improve your financial health and freedom.

What is a credit score?

Your credit report is the combined history of any financial activity your credit account issuers (including for loans, mortgages, and credit cards) report to one of the three major credit bureaus (Equifax, Experian, and TransUnion). Most of your financial activity — from making purchases with your credit card to paying down your balance — contributes to your credit report and determines your credit score.

What is a FICO score?

Your FICO credit score is the 3-digit score that creditors use to assess your creditworthiness. FICO, or the Fair Isaac Corporation, is an analytics company with one of the most commonly used credit scoring models (aside from VantageScore). To calculate your score, FICO factors metrics like your payment history, credit usage, and the length of your credit history.

Your resulting score is what lenders and financial providers use to determine your borrowing qualifications for credit cards, loans, and mortgages. Since your credit score is tied to your credit report, if a lender or loan officer ever reviews your credit report, they’ll see your most recent FICO score.

Having a low credit score or no score at all signals to lenders that you have little experience with credit and may be riskier to lend to. This can make it difficult to get certain loans or credit opportunities. While lenders may not deny your credit applications outright, they may offer reduced credit limits or smaller loan amounts as a reaction to that risk. Your FICO score also determines your eligibility for most financial assistance, including auto loans and mortgages.

What is a credit report?

A credit report is a detailed personal report that has your credit history broken down into individual events. Every time you apply for a loan, open a new credit card, or make a payment (or miss payments), creditors record those events on your report. This collective financial activity determines your credit score.

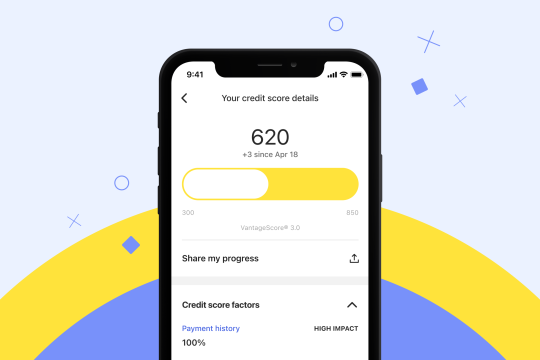

Your credit score updates monthly, but you can check your report any time with EarnIn’s Credit Monitoring tool. Knowing your score will help you make sure you’re on track to improving it.

How does credit reporting work?

A full credit report contains personal information, like your name and social security number, as well as public records, like your home address and owned properties. It also includes your history of opened and closed credit lines, debt payment history, and much more.

Every month, you’ll receive an updated credit report with new data from the three major credit bureaus and your latest FICO score. If you want to keep tabs on your report and any fluctuating variables, you can use a credit monitoring tool.

Your credit report will cover all your credit scoring events, and these events fall into one of two categories:

-Revolving loans: Credit cards, installment loans, and other forms of borrowed money.

-Service accounts: Utility bills, service bills, and other financial events that may impact your credit.

Typically, anything you do concerning revolving loans goes on your credit report. The records of these transactions will show your credit application dates, approval statuses, and payment information. As for service accounts, these don’t automatically appear on your credit report. If you do want them recorded, you would have to use a third-party reporting service, like Experian Boost, to list them on your report.

Credit score strategies

As a general rule, every event or update to your credit report affects your credit score, but it does help to know what bills help build credit ratings. You can improve or impact your credit score in two ways:

-Building a long-standing history with good faith and on-time payments.

-Triggering events that update your credit report, like applications and credit checks.

Some of the best strategies for boosting your score involve following basic financial tactics, like taking out a loan and paying it back over time. You can also open a small line of credit, like a limited credit card, to make smaller purchases and pay off your balance in full each month until your credit rating and history improve.

Are utility bills reported to the three major credit bureaus?

The major credit unions consider utility bills to be a “service account,” so they don’t list them on your credit report. If you’re wondering whether utility bills affect credit scores or if paying utilities can build credit, the answer is usually no — unless you use Experian Boost or another third-party service to add those payments yourself. These extra services add household utilities and bill payments to your credit report to help improve your score.

Many people also wonder if a phone bill builds credit, to which the answer is also no. Wireless providers don’t report payments to the credit bureaus, so your phone bill will not help you build credit. That said, any negative events will appear on your credit report, like failure to pay, which can hurt your credit score.

What bills affect your credit score and help build credit?

The bills that affect your credit score fall into one of two categories: automatic and third-party. Automatic bills will also always show up on your credit report, including payment histories, but third-party bills won’t. A great third-party example is medical bills. If you miss payments on your medical bills, that can impact your credit score negatively, but if you make timely payments on them, they won’t show up on your credit report or change your credit score.

Automatic

-Auto loans: Payment history for auto loans includes on-time payments, which have a positive impact, and missed payments, which negatively affect your score.

-Student loans: As with auto loans, student loan payments can drive your score up or down, depending on if you keep up with your payments or fall behind.

-Credit cards: Applying for credit cards, receiving limit increases, and making on-time payments all affect your credit score positively. Meanwhile, your creditors will share any missed payments and delinquent accounts (overdue accounts with missed payments past the due date) with the three credit bureaus, which can cause a drop in your credit score.

-Medical bills: Most healthcare providers don’t report medical bills and payments, but if you have outstanding debts and they go into collections, they may report those delinquencies, which will negatively affect your credit score.

Third-Party

-Rent: Consistent rent payments only appear on your credit report if a landlord uses a third-party service, but late payments or delinquencies do go on your report.

-Utility bills: Your creditor report doesn’t factor utility bills unless they’re delinquent.

How important is my payment history?

Your payment history accounts for about 35% of your credit score, while your credit utilization (ratio of your credit card balances to your credit limits) makes up 30%. This means paying your bills on time and keeping your balances to a minimum can greatly impact your score. If you’re able to pay off a credit account entirely, know that it may briefly drop your score, but it also signals responsible debt settlement and will improve shortly after.

Also, if you discover you have a negative credit card balance, don’t panic. This simply means you overpaid your balance. The credit card issuer might give you back your overpayment, or they’ll apply the amount toward any future charges you make with your card. Either way, there are no negative effects on your score for overpaying — only underpaying.

Having no payment history will leave you without a score, and having a poor payment history will leave you with a poor score. On the other hand, if you have a good payment history, you’ll likely have a good score — as long as your credit utilization rate isn’t too high. Keeping your payment history up-to-date is essential for maintaining your credit.

Track your credit for free with EarnIn

Making on-time payments and checking your credit report regularly are two of the best ways to build stronger credit. EarnIn can help you with both.

By using EarnIn’s free Credit Monitoring tool right on the EarnIn app, you can review everything on your credit report, keep an eye out for any changes, and track your score improvement. You can also take advantage of EarnIn’s Cash Out tool, which lets you access your pay as you work — up to $100 per day or $750 every pay period with no interest, no credit checks, and no mandatory fees., This can help you keep up with your bills and continue to build good credit with consistent payments. Download EarnIn today and get financial tools that can help you reach your goals.

You may enjoy

EarnIn is a financial technology company not a bank. Subject to your available earnings, Daily Max and Pay Period Max. EarnIn does not charge interest on Cash Outs. EarnIn does not charge hidden fees for use of its services. Restrictions and/or third party fees may apply. EarnIn services may not be available in all states. For more info visit earnin.com/TOS.